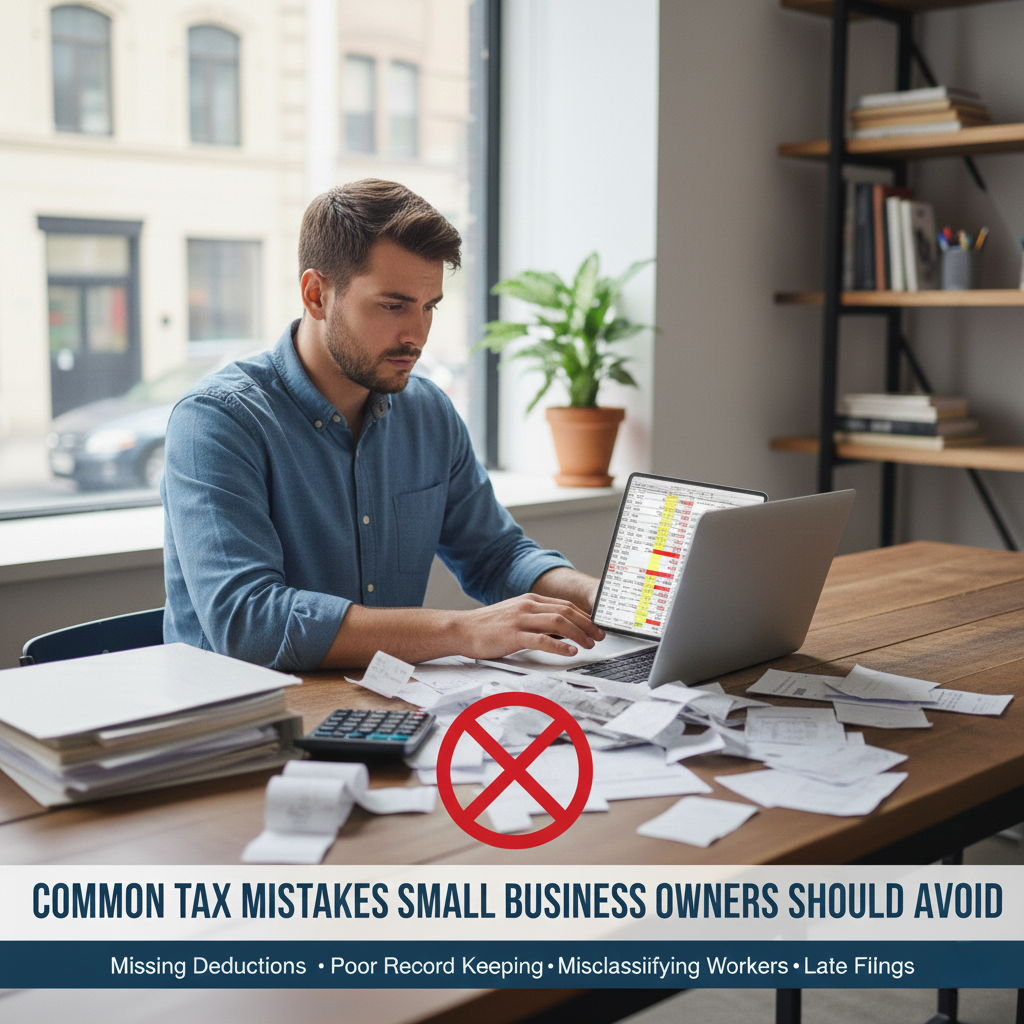

Tax compliance is a major responsibility for small business owners, yet mistakes are common and often costly. Understanding these pitfalls can help you stay compliant and avoid unnecessary penalties.

Mixing Personal and Business Finances

One of the most frequent mistakes is combining personal and business expenses. This makes recordkeeping difficult and increases the risk of errors during tax filing.

Maintaining separate bank accounts and credit cards for business use simplifies bookkeeping and ensures accurate financial reporting.

Poor Recordkeeping

Incomplete or disorganized records can lead to missed deductions and filing delays. Receipts, invoices, and bank statements should be stored and categorized consistently throughout the year.

Accurate bookkeeping ensures your tax filings are based on reliable information and reduces the risk of audits or penalties.

Missing Deadlines

Late tax filings or payments can result in penalties and interest. Many business owners struggle to keep up with multiple deadlines throughout the year.

Working with a professional and maintaining organized records helps ensure deadlines are met on time.

Overlooking Deductions

Many small business owners miss out on deductions simply because they are unaware of them. Commonly overlooked deductions include home office expenses, vehicle usage, software subscriptions, and professional services.

Regular bookkeeping and professional guidance help identify eligible deductions and maximize tax efficiency.

Not Planning Ahead

Taxes should not be an afterthought. Without planning, business owners may face unexpected tax bills.

Year-round bookkeeping and tax planning allow you to estimate liabilities, set aside funds, and avoid surprises. This proactive approach helps protect your cash flow and financial stability.

At Elite Aid Bookkeeping & Tax Services, LLC, we help business owners avoid these mistakes by combining accurate bookkeeping with reliable tax support.